Syria’s wheat harvest season is underway, with grim projections of severe shortfalls resulting from drought, regime mismanagement and surging prices for agricultural inputs. While the Syrian regime announced an increase in its purchase price for wheat, its rate remains lower than that of the Self-Administration and far lower than black market rates and as such, is expected to resort to coercive measures to pressure farmers into selling their crop to the regime. Regardless of its efforts to secure domestic crop, the regime still needs to import wheat to make up for the shortfall, an increasingly unviable option given the regime’s difficulty with financing imports and skyrocketing global grain prices. Amidst these food and fuel shortages, the regime is ploughing ahead with devastating austerity measures compounding the misery and hardships faced by ordinary Syrians. Most Syrian families have already been making crucial survival decisions over which essentials to cut, choosing between food, medicine or their children’s education. These negative coping mechanisms will only be further exacerbated by the current conditions. The economic devastation that is being wreaked on Syria is entrenching extreme poverty rates among the country’s population; meanwhile, the Assad regime is ramping up massive revenues through its narco-state activities, severely limiting Syria’s prospects for any sort of recovery.

Economic Indicators

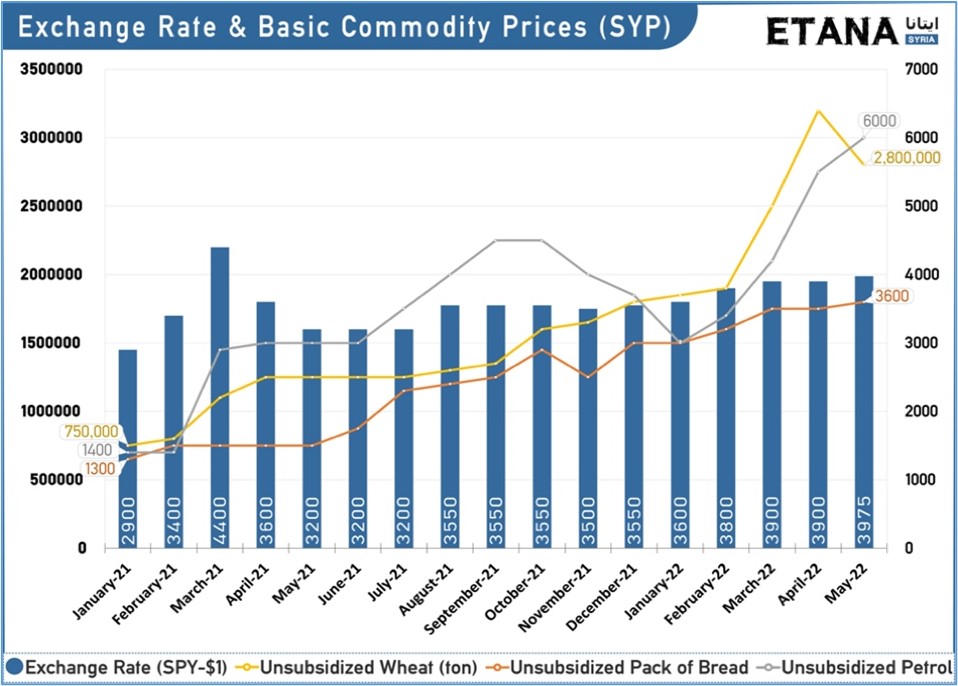

- Exchange rate: Despite a deepening budgetary crisis accelerated by sharply rising fuel and food prices, the Syrian pound (SYP) has remained relatively stable since the beginning of May 2022, at around 4,000 SYP to the dollar. The regime has continued to restrict circulation of the Syrian currency, striving to maintain a balance of supply and demand and prioritize stability in the exchange rate despite the loss of purchasing power among the Syrian population. However, compared to a year ago, the currency has depreciated by 25%, pushing Syrians into deeper poverty as their purchasing power continues to plummet.

- Wheat:

-Harvest: Syria’s wheat harvest season has kicked off with prospects for this year’s yield remaining grim due to drought, climate change, corruption, regime mismanagement and skyrocketing prices of inputs including fertilizer and fuel following Russia’s invasion of Ukraine. Regime authorities were counting on covering the basic needs of the Syrian population through grain imports from Crimea. While there are reports that Russia has sold wheat stolen from Ukraine to Syria in recent weeks, the volume of wheat needed far exceeds any purchases of purloined grain.

-Purchase price: The regime raised the purchase price of wheat to 2,000 SYP per kilogram for areas under its control and 2,100 SYP per kg for areas outside of its control, primarily targeting farmers in Self-Administration areas in the north-east. Following the regime’s announcement of the increase in the purchase price, the Self-Administration set its wheat purchase price to 2,200 SYP per kg. In contrast, black market prices are averaging around 2,800 SYP, presenting an enticing alternative for farmers. The result is that very little grain grown in north-east Syria is likely to enter regime silos, compounding an increasingly alarming food crisis as shortages grow more acute over the course of the year.

-Coercion: In light of shortages from failed agriculture policies, surging prices that the regime can ill afford to pay and formidable import barriers related to Russia’s invasion of Ukraine, the regime is looking to security forces and a planned campaign of intimidation to coerce farmers into handing over grain yields to authorities. Given the limits of brute force and strategies farmers are already employing to conceal the true volume of harvest yields, this emerging strategy may result in some extra seizures but is almost certainly poised to fall short of its objectives.

Regime Mitigation Measures

- Austerity measures:

-Subsidy cuts: The Russian invasion of Ukraine and the ongoing surge of inflation are further destabilizing the regime’s budget projections for this year, adding a new urgency to cut costs and further reduce benefits to the Syrian population.

-Fuel prices: In May, the regime announced a series of price hikes on fuel items across the board. Diesel rose from 1,700 to 2,500 SYP; 90-octane gasoline from 2,500 to 3,500 SYP; and 95-octane from 3,000 to 4,000 SYP. Fuel allocations were also reduced for all regions of the country by rates ranging from 30 to 50%, which the regime justified by pointing to slumping import volumes to Syria. Black market prices in the meantime have ballooned to over 6,000 SYP. Fuel price increases are having a particularly pronounced impact on the population, increasing costs for all other products as a result of rising transport and production costs.

-Electricity: While utility costs remained unchanged, this is because an increase in electricity bills would begin eclipsing the average monthly income––an issue that is already resulting in most bills going unpaid. However, the regime is reducing electricity expenditures by further reducing hours of service. Syrians will now receive only three hours of electricity per day, forcing them to either rely on private generators or go without electricity for the remaining 21 hours. It is also likely that the price of a kilowatt will be raised to 500 SYP for industrialists during the coming days.

-Cement: The regime announced a hike for cement prices in May, increasing the cost from 240,000 to 414,000 SYP per ton, a jump of nearly 70%. This coincided with a rise in the price of concrete on the black market to 700,000 SYP per ton, the highest price ever recorded in Syria. This change is being driven in large part by rising production costs for concrete and is likely to also accelerate a rise in the price of other building materials.

-Public sector salaries: Another striking sign of the acute financial crisis gripping the regime in recent months has been the failure of authorities to pay public sector employees for the month of April. Employees were instead informed that the amount would be transferred to the salaries of the month of May as authorities stalled for time. - Telecommunications:

-Price hikes: The regime has increased user fees for Syrian telecom operators MTN, Syriatel and Syrian Telecom by 50%, bringing costs to a minimum $9 USD per month for most users. This is a formidable sum for most Syrians when the average public sector salary is around $40 and comes atop surging prices for other goods and services. The move will inevitably force many to find alternative solutions, such as sharing lines.

-Infrastructure challenges: Telecom companies are currently operating at a steep financial loss, and the recent price hikes are unlikely to alter that picture. Additionally, operators are increasingly struggling to provide service to many areas under regime control, due to the deteriorating electricity situation in the country and widespread theft of telecom infrastructure.

Regime Allies & Neighboring Countries

- Iran:

-Credit line: In a surprise visit to Tehran in early May, Bashar al-Assad signed an agreement with Iran to open a new credit line for Syria to support the purchase of fuel and other basic goods. While Iranian oil shipments have continued to arrive at Syrian ports since the last credit line dried up in 2018, they have been less consistent and unable to meet Syrian needs. The value of the credit line is yet to be announced and it remains to be seen whether Iran will be able to deliver a more consistent fuel supply in the coming months.

- Jordan:

-Nassib: Trade volumes across the border with Jordan remain low, despite a concerted push by the Syrian Chambers of Commerce to ramp up exports of certain items––particularly agricultural products like olive oil, onions and garlic. Despite these efforts, the most consequential exports into Jordan remain hashish and other narcotics, particularly Captagon. As Syrian-produced drugs have continued to flood the Jordanian market, oftentimes hidden in fake agricultural products, restrictions on Syrian imports put in place by Jordan remain in force, dimming the prospects for any significant uptick in trade in the near future.